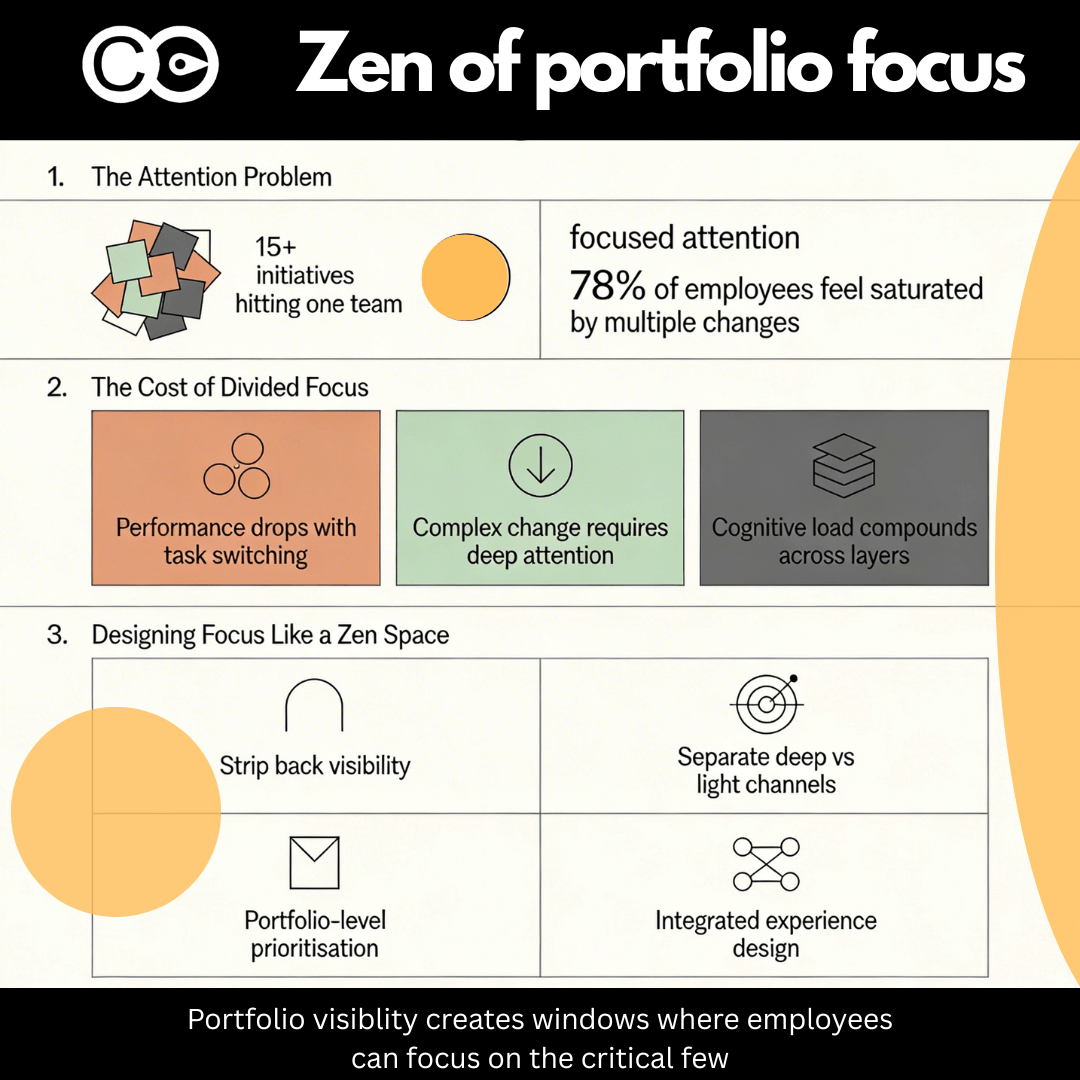

Financial services firms are not just “going digital” – they are running overlapping waves of highly specific transformations that rewrite how risk is managed, products are delivered, and work gets done. Research from BCG and McKinsey shows that banks and insurers that treat these as a managed portfolio, backed by clear behavioural expectations and data, deliver significantly better outcomes than those that approach each program in isolation. Prosci’s work in financial services further reinforces that projects with strong change management are multiple times more likely to meet or exceed objectives, particularly where leaders and middle managers are visibly engaged.

Below are the most common transformation types in financial services, the specific change management challenges they create, and concrete tactics you can apply straight away. The focus is on behaviour change, the pivotal role of middle managers, disciplined portfolio management, and data and tracking that go far beyond simple status reporting.

The eight transformation archetypes in financial services

Across major banks, insurers, and wealth managers, transformation activity tends to fall into a repeatable set of archetypes, regardless of geography.

- Regulatory and risk transformation

- Core systems and architecture modernisation

- Customer, product, and distribution transformation

- Operating model and cost transformation

- Finance and performance management transformation

- Data, analytics, and AI transformation

- Culture, leadership, and ways of working

- Sustainability and ESG transformation

Each of these requires different change tactics in practice, even though they often compete for the same people, customers, and operational bandwidth.

1. Regulatory and risk transformation

Examples include major AML and KYC uplifts, operational resilience programs (such as CPS 230 style requirements), conduct risk remediation, and Basel or capital and liquidity changes.

Typical change management challenges

- Compliance fatigue: Staff feel there is always another policy, training, or control, which can drive surface-level completion without genuine behaviour change.

- Fragmented ownership: Risk, compliance, operations, and product all run “their” reg programs without a single view of impacts on customers and staff.

- Middle manager overload: Line managers are the ones chasing attestations and juggling rosters for training, but rarely see the full picture of what their people are experiencing across the portfolio.

Practical tactics and strategies

- Start with a regulatory change portfolio view, not a single project charter

- Create a simple but comprehensive register of all in-flight and planned regulatory changes, with columns for impacted segments, business units, timeframes, and required behaviours (for example, “always verify source of funds for X category”).

- Visualise this as a heatmap by team or branch so middle managers can see when their people are being hit from multiple directions at once.

- Translate regulations into a small set of observable frontline behaviours

- Instead of leading with policy clauses, define 5 to 10 behaviours per initiative that are easy to observe in the field, such as “no account opened without documented beneficial owner verification”.

- Train middle managers to coach against these specific behaviours and to log what they see weekly in a simple tool or platform. This creates a feedback loop that is much richer than generic training completion data.

- Use middle managers as co-designers, not just messengers

- Hold short design sessions by segment (for example, branch leaders, contact centre leaders) to jointly simplify processes and scripts that meet both regulatory and operational needs.

- Research on change in banking shows that when line managers feel they have shaped the solution, adoption and sustainment rates rise markedly compared with purely top-down designs.

- Track “real” compliance through behaviour and outcome metrics

- Combine leading indicators (observation checklists, targeted QA, mystery shopping) with lagging indicators (breach numbers, near misses, remediation volumes).

- Use a portfolio dashboard to compare teams and regions, then direct support and coaching where variance is highest rather than applying blanket training.

2. Core systems and architecture modernisation

This includes core banking or policy administration replacements, payment rail upgrades, and large-scale cloud and integration programs.

Typical change management challenges

- The impact is often underestimated: core changes alter hundreds of micro behaviours such as how exceptions are handled or how data is captured.

- Go live dates are treated as the finish line even though research by McKinsey shows that value realisation often lags well beyond technical cutover in financial institutions.

- Middle managers are asked to handle extra work during migration at the same time as hitting BAU efficiency and risk targets.

Practical tactics and strategies

- Build a process impact catalogue that middle managers can own

- Map each process affected by core changes and assign a named operational owner, typically a middle manager or team leader.

- For each process, define specific behaviour changes, such as “use system workflow instead of offline spreadsheet”, and how they will be measured (for example, utilisation of new paths, rework rates).

- Use sequential “dress rehearsals” that focus on behaviours, not just technology

- McKinsey’s research on technology transformation in financial services highlights the value of iterative testing in realistic conditions before full cutover.

- Run rehearsals where real users process real or realistic work items end to end in the new system. Capture not only defects but also where people attempted to revert to old workarounds, and feed this back to middle managers as coaching material.

- Give middle managers a short, structured playbook for stabilisation

- Provide a stabilisation playbook that includes standard daily huddles, defect and workarounds logging templates, and a simple decision guide on what can be fixed locally versus escalated.

- Track stabilisation metrics such as transaction turnaround time, error rates, and staff confidence scores by team, not only at program level, so support can be targeted quickly.

- Tie portfolio decisions to operational capacity and risk appetite

- Use the change portfolio to decide whether to pause or slow less critical initiatives in the same period so middle managers are not overwhelmed during cutover and stabilisation.

- This is where tools that can visualise initiative overlaps, change saturation, and operational risk at a portfolio level are particularly valuable.

3. Customer, product, and distribution transformation

Examples include end-to-end journey redesigns for onboarding, lending or claims, open banking and ecosystem plays, and repositioning of wealth or insurance propositions.

Typical change management challenges

- Competing priorities between customer experience, revenue, and risk objectives.

- Channel conflict: frontline distribution leaders may fear losing volume to digital or partner channels.

- Behaviour change is subtle: the same journey may exist, but the tone, sequencing, and use of data in interactions are different.

Practical tactics and strategies

- Make a journey portfolio and clarify the “north star” (or Southern Cross for us in the southern hemisphere) for each

- Identify your key journeys and map which initiatives touch each one in the next 12 to 24 months.

- For each journey, define a small set of target behaviours at manager and staff level, for example “always check eligibility in the new tool before discussing price” or “offer digital completion as default, not exception”.

- Give middle managers ownership of journey performance, not just channel metrics

- Provide them with an integrated data view of their customers’ journey, such as abandonment points, complaint themes, and NPS, not just product sales volumes.

- Prosci’s work shows that when direct managers can see clear cause and effect between new behaviours and improved outcomes, they are much more likely to coach and reinforce those behaviours consistently.

- Use small experiments with clear behavioural hypotheses

- Rather than rolling out a single script or process nationally, test two or three alternative behaviours in small pilots and measure the impact on both customer and risk outcomes.

- Middle managers should be directly involved in choosing which variant to scale and in sharing practical stories with their peers on what worked and why.

- Track experience and adoption through both quantitative and qualitative data

- Supplement NPS and conversion metrics with quick frontline and middle manager pulse checks focused on questions such as “what is getting in the way of using the new journey consistently”.

- Use this data in fortnightly or monthly portfolio reviews where you decide whether to double down, adjust, or stop specific initiatives touching each journey.

4. Operating model and cost transformation

Typical examples are zero-based cost reviews, shared service consolidation, offshoring or nearshoring of operations, and enterprise agile or product model shifts.

Typical change management challenges

- Perceived as cost cutting rather than value creation, which triggers defensive behaviours and talent flight.

- Middle managers are squeezed between efficiency targets and expectations to support their people through change.

- Benefits often erode over 12 to 24 months if behaviours drift back to old patterns once scrutiny eases.

Practical tactics and strategies

- Make benefits and behaviour explicit in the portfolio ledger

- For each initiative, identify target benefits (for example, 20 per cent reduction in manual handling) and the specific behaviours required to sustain those benefits, such as “route 95 per cent of claims through straight through processing”.

- Track both in the same dashboard and review monthly with operational leaders and finance so there is a shared understanding of progress and slippage.

- Give middle managers a clear deal: support in exchange for ownership

- Research into transformation programs finds that where managers are given clarity about their role, additional support such as coaching or extra resources, and recognition for benefits delivery, they are more likely to own difficult trade offs.

- Make it explicit that success is not just “hitting the savings number” but embedding new ways of working in team routines, and track their performance against both dimensions.

- Use data and stories together to rebuild trust

- Publish regular, transparent data on how operating changes are affecting service levels, risk incidents, and staff engagement.

- Encourage middle managers to bring forward examples where a new operating model led to better customer outcomes or staff development, and use these stories in broader communication to avoid a purely cost narrative.

5. Finance and performance management transformation

This includes moving to rolling forecasts, implementing new profitability and capital allocation models, and automating finance processes such as record to report and procure to pay.

Typical change management challenges

- Strong professional identity among finance teams built around existing tools and methods.

- Stakeholders outside finance may see new performance frameworks as opaque or unfair.

- Middle managers in business units may not be equipped to interpret new metrics and adjust behaviours accordingly.

Practical tactics and strategies

- Co-design new performance narratives with business managers

- Rather than simply issuing new dashboards, hold short design workshops with middle managers from the front line, operations, and support functions where they test drive the new metrics using real scenarios.

- Ask explicitly “what decisions would you make differently with this information” and refine the design until those decisions are clear and actionable.

- Track decision quality, not only forecast accuracy

- Research into finance transformation highlights that the real value comes from better, faster decisions, not only more efficient forecasting cycles.

- For major decisions, such as pricing changes or capital allocation shifts, log whether the new data and tools were used and whether outcomes improved relative to prior approaches. Feed this back into coaching for both finance and business leaders.

- Equip middle managers with simple “metric to behaviour” guides

- Produce short guides that link each key metric to two or three concrete behaviours. For example, if a branch profitability measure now includes risk-adjusted capital, suggest specific actions like “rebalance lending mix” or “target fee leakage in particular segments”.

- Monitor usage of these guides through manager feedback and pulse surveys, and refine them based on real examples from the field.

6. Data, analytics, and AI transformation

Financial institutions are investing heavily in data platforms, self service analytics, and AI for use cases such as fraud detection, credit decisioning, and personalised marketing.

Typical change management challenges

- Significant trust issues: staff may not understand how models work or may fear being replaced.

- Shadow solutions: teams revert to spreadsheets or legacy reports if new tools are hard to use.

- Ethics and risk questions that cut across many parts of the organisation.

Practical tactics and strategies

- Treat analytics and AI initiatives as a single, governed portfolio

- Maintain a central register of models and analytics products that records owners, stakeholders, risk level, and intended user behaviours (for example, “check AI recommendation first, then apply judgement”).

- Use this to identify where the same people are being targeted by multiple tools and to coordinate training and communication.

- Focus on building data literacy via middle managers

- Prosci and others emphasise that direct supervisors are the strongest influence on individual adoption of new ways of working in financial services.

- Train middle managers in basic concepts such as data quality, bias, and model limitations, and equip them with talking points and scenarios so they can explain tools to their teams in practical, contextualised language.

- Monitor adoption at granular levels and act fast on early signals

- Integrate ethics and model risk into everyday behaviour expectations

- Reinforce that challenging or overriding a model when it does not make sense is a desired behaviour, not a failure.

- Track and review override patterns in governance forums, and surface positive examples where human judgement improved outcomes.

7. Culture, leadership, and ways of working

Many financial services firms are moving to more agile, customer centric, and data driven cultures, often supported by new leadership frameworks and people processes.

Typical change management challenges

- Culture is often treated as a separate workstream rather than something woven through each transformation.

- Middle managers receive high level values statements but little practical support on how to change their own daily behaviour.

- Progress is hard to quantify without robust measures.

Practical tactics and strategies

- Anchor culture change in a small set of observable leadership behaviours

- Equip middle managers with routines that embed cultural behaviours

- Use pulse surveys and qualitative data as serious inputs to portfolio decisions

- Research into transformation suggests that employee sentiment is a leading indicator of whether change will stick.

- Integrate sentiment and behavioural data into your portfolio dashboards alongside financial and delivery metrics, and be prepared to slow or reshape initiatives where signals are deteriorating.

8. Sustainability and ESG transformation

Banks and insurers are reworking portfolios, risk frameworks, and disclosures to meet rising expectations around climate and social responsibility.

Typical change management challenges

- Perceived as compliance or marketing rather than core to strategy.

- Complex, cross-cutting metrics that middle managers may find abstract.

- Potential tension between short term financial targets and long term ESG goals.

Practical tactics and strategies

- Connect ESG targets to day to day portfolio decisions

- Give middle managers practical decision tools

- Provide simple decision trees and case examples that show how to apply ESG policies in realistic client situations, such as when to escalate a lending decision related to high emission sectors.

- Track how often managers use these tools and collect feedback on where policies or guidance are unclear.

- Report ESG progress alongside traditional financial metrics

Making portfolio management, the work of middle managers, and data work together

Across all eight archetypes, three levers consistently differentiate successful financial services transformations from those that disappoint:

- Active, data led change portfolio management: A single, integrated view of initiatives, impacts, timing, and risks that is used to make real trade off decisions.

- Empowered, equipped middle managers: Line managers who understand the why, have clear behavioural expectations for their teams, and are given the tools and time to support change.

- Rich, behaviour focused data and tracking: Moving beyond activity counts and training completions to observable behaviours, sentiment, outcome measures, and feedback loops at team level.

Firms that approach change in this integrated way are better able to handle the intensity and complexity of modern financial services transformation and to sustain benefits beyond the life of individual programs.

Platforms like The Change Compass illustrate how portfolio level insights, operational data, and change metrics can be combined to support these practices in a systematic way across financial services organisations.

Frequently asked questions

How do we practically start with change portfolio management if we are currently project centric?

Start by building a simple central register of all significant initiatives with fields for impacted business units and customer segments, timing, and estimated people impact. Use this in a monthly forum with senior and middle managers to review hotspots, adjust timing, and agree priorities.

What should middle managers in financial services focus on first when there are many concurrent changes?

Research and practice suggest that middle managers create the most value when they focus on clarifying expectations for their teams, coaching observable behaviours linked to outcomes, and escalating systemic issues that individual teams cannot fix alone.

Which metrics are most powerful for tracking behaviour change during transformation?

A balanced set usually includes leading indicators such as adoption and utilisation of new tools or processes, observation or QA scores of key behaviours, and employee sentiment about specific changes, combined with lagging indicators such as customer outcomes, risk incidents, or process performance.

How can we make research and data resonate with senior leaders who are sceptical about change management?

Use a small number of solid external references, such as Prosci and McKinsey studies on success rates in transformation, alongside your own internal data to show the relationship between strong change practices, risk outcomes, and financial performance.

Where can we find more detailed examples tailored to financial services?

Industry specific insights and case based guidance are increasingly available from consulting firms and specialist platforms. For example, The Change Compass knowledge hub focuses on how financial services organisations can use change data and portfolio analytics to plan and deliver complex transformations more effectively.